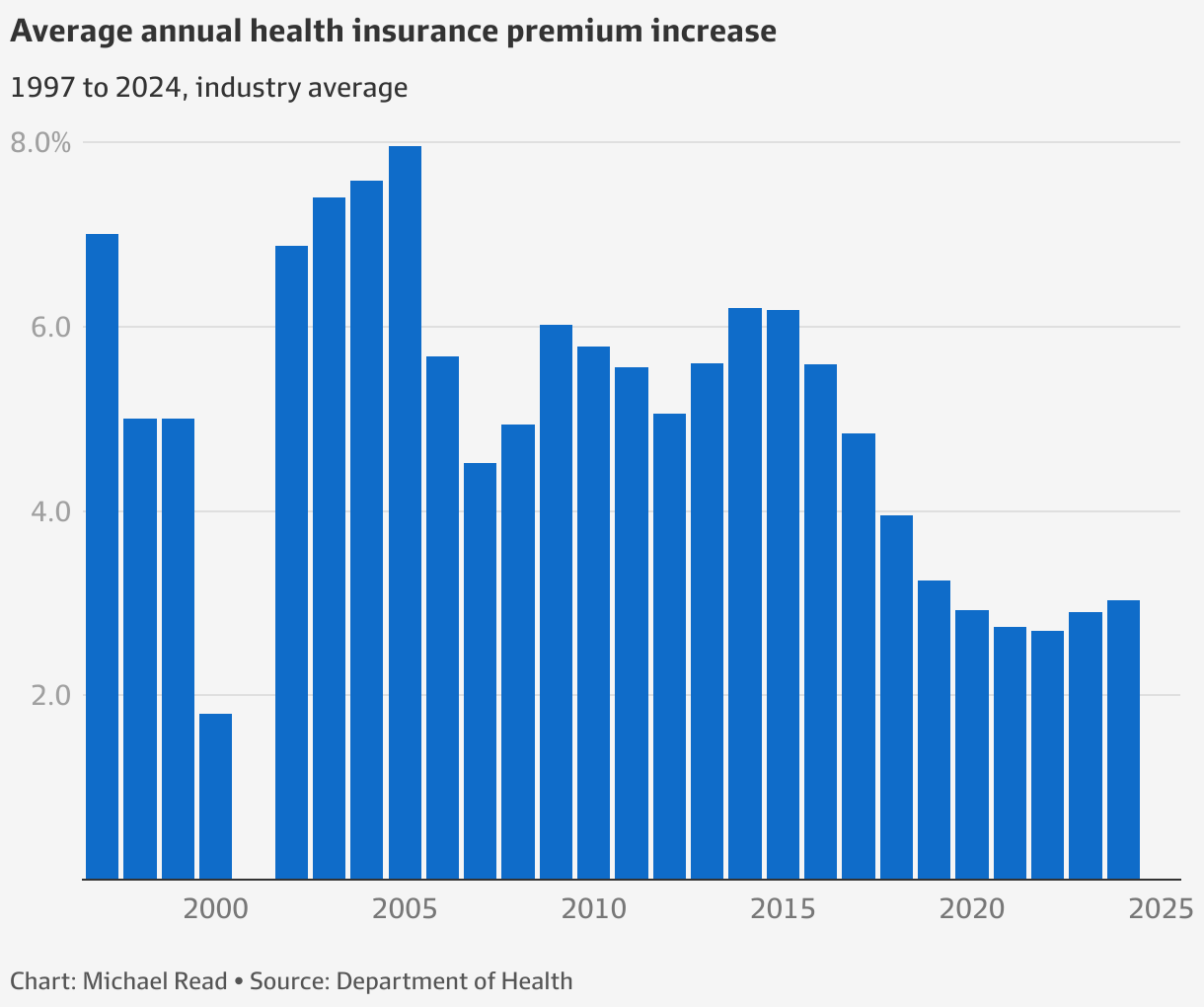

NIB CEO Mark Fitzgibbon tips private health insurance premiums to rise 2 to 3 per cent in 2023

The looming announcement arrives at a time when households are grappling with Australia’s most acute inflation outbreak in a era and fast climbing curiosity costs.

Permitted high quality increases will arrive into effect on April 1.

Using the pandemic wave

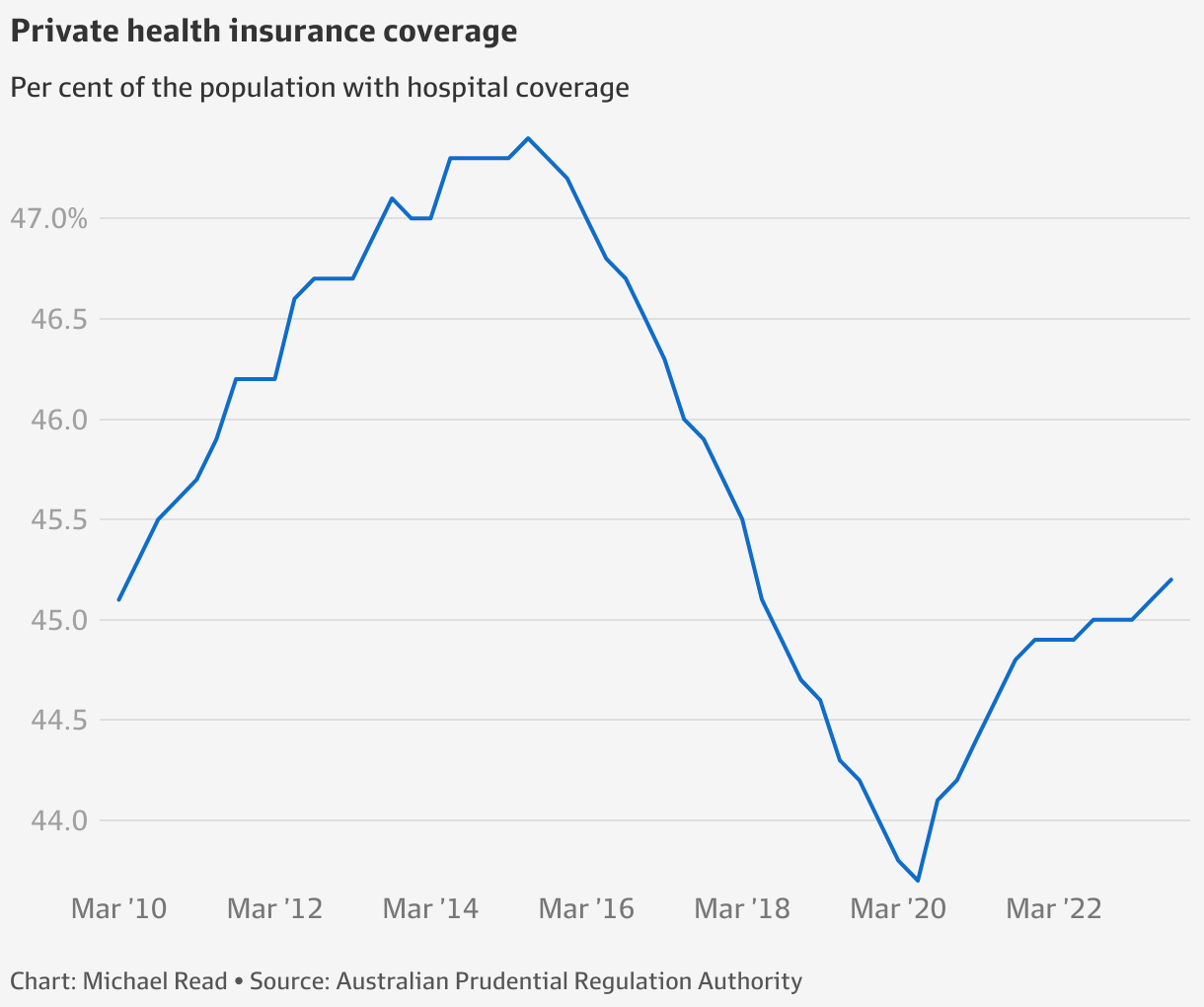

The pandemic was a boon to insurers’ bottom-lines, with fewer individuals earning statements due to a pause on elective surgical procedure, major the sector to build up significant hard cash reserves.

Personal health insurers are also having fun with a membership rebound, as a blowout in public hospital wait occasions pushes a lot more Australians into the procedure.

About 758,000 Australians have signed up for personal health coverage considering that September 2020, in accordance to data from the Australian Prudential Regulation Authority (APRA), and personal health and fitness insurers have witnessed nine consecutive quarters of membership development.

Mr Fitzgibbon said wellness insurers experienced compensated users by giving funds returns and extending address for COVID-linked remedies.

“I believe it demonstrates the field is in fantastic condition at the moment, and the sector is doing the job really dutifully towards trying to keep premiums affordable and compensating users for the downturn in activity during COVID.”

MST Marquee health care analyst Andrew Goodsall mentioned he was also hearing of proposed quality will increase in the 2 to 3 for every cent vary.

Even though health care prices are raising, putting upward tension on rates, insurers are anticipated to draw down from their funds reserves, holding rates in verify.

“The even larger picture is that health care is going to carry on to have upward strain on price tag, and insurers want to try out to assist the business find out how it can discover price savings that really do not affect affected person results,” Mr Goodsall stated.

Non-public Health care Australia chief government Rachel David stated she expected high quality boosts to appear in “well under” the typical rate of inflation.

Individuals slow to reconnect

Dr David said insurers have been not observing people rebook deferred surgeries, maintaining stress on premiums down.

“Patients [have been] extremely gradual to reconnect with the system right after the pandemic due to complacency and worry of catching COVID,” Dr David told AFR Weekend.

“Now we are observing that commence to get better now, but what we’re not observing is folks rebooking for surgical procedures.”

Reasonably subdued growth in activity is counteracting upward strain on rates, which Dr David explained was coming from the contracts negotiated in between insurers and hospitals.

“Anything in a contract that is been negotiated in the previous 18 months is likely to be matter to the similar inflationary pressures as any place else in the financial system,” Dr David explained. “Hospitals are matter to big spikes in recruitment costs, the prices of electrical power and power, and the expense of meals.

“And regrettably, we are nevertheless seeing the price of generic clinical products – the price tag per treatment – growing out of proportion to the selection of procedures done.”

Looming slowdown

An economic slowdown could place an close to the private wellbeing revival.

Dr David said one particular of the big hazards to insurers was that consumers will cancel their policies as value of living pressures pressure them to make cutbacks.

“Whenever we survey associates, the premium cost often arrives back again as their significant issue. And for homes, usually, personal health and fitness insurance coverage has been the second-premier expenditure right after their lodging fees.”

Mr Goodsall stated extended public hospital waiting lists intended shoppers will be much less most likely to reduce back on private health and fitness insurance include as value of dwelling pressures mount, with surveys demonstrating worries more than accessibility to treatment were being a significant driver of domestic selection-producing.

“I consider people would only drop coverage if they felt like they just definitely didn’t need it, but put up COVID, general public medical center surgical procedures waitlists are at all-time highs, so that is less likely” he explained.